19 May 2026

H2 Estimates Record Betting on FIFA World Cup 2026

The 2026 FIFA World Cup will kick off on 11 June 2026, with the final set for 19 July 2026. This edition will mark the first World Cup jointly hosted by three nations, with the United States returning as host for the first time since 1994, which still holds the record for the highest total attendance at any World Cup. Mexico will become the first country to host the tournament three times, while Canada will host a men’s World Cup for the first time.

The tournament will also be the first to feature an expanded field of 48 teams, up from 32, resulting in a total of 104 matches – 40 more than any previous edition. This expansion significantly increases the addressable betting opportunity, providing operators with a broader slate of events through which to engage audiences. Nevertheless, it is important to exercise caution in projecting betting activity. The increased number of fixtures, combined with the inclusion of lower-ranked teams, may dilute engagement, especially in the early stages of the competition.

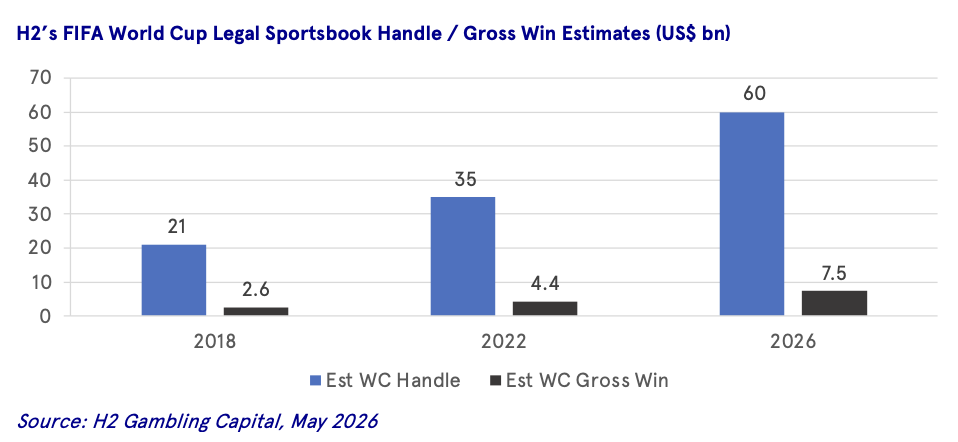

Based on our analysis, H2 estimates that c.$60bn will be wagered on the 2026 FIFA World Cup through legal sportsbooks, representing a 71% increase over our estimates for the 2022 tournament and a 185% increase compared with 2018. These estimates reflect legal sportsbetting channels only and do not incorporate illegal or unregulated markets. This uplift is broadly consistent with observed tournament data from regulated markets; France’s national gambling authority (ANJ) reported that online stakes on the 2022 World Cup were 56% higher than the 2018 edition, providing external validation of the scale of uplift a major tournament can generate. However, the uplift is also a function of more regulated markets, as Brazil (amongst other markets) is included in the estimates for the first time, following regulation of the market in 2025.

Of this, we estimate $5.7bn will be wagered across the host nations. Mexico is expected to have the highest soccer share of betting spend, followed by Canada, with the US the lowest — however, given its market size, the US will be the greatest contributor at $2.9bn of handle, compared to $2.5bn in Mexico and $0.3bn in Canada (legal sportsbooks only, excluding dot-com sites). To put that into context, the US generated c.$1.3bn of soccer handle across June and July combined last year.

Tournament Format & Betting Implications

The World Cup is seen as a major customer acquisition tool for operators. For example, during the 2022 World Cup, French operators saw the addition of 177,000 new unique players, while Belgium saw 43,000 new unique players. At a high level, the expanded 2026 World Cup extends the betting opportunity across more matches and more nations.

However, a more detailed assessment suggests that the expansion is unlikely to translate into a proportionate increase in wagering activity. 60% of the additional fixtures are in the group stage, where engagement is typically lower. The inclusion of a larger number of lower-ranked teams is also likely to reduce the average quality, interest and competitiveness of matches, with a greater prevalence of one-sided fixtures and matchups without leading nations. The remaining incremental fixtures are introduced through the addition of a new Round of 32 stage. While these matches will generate higher levels of engagement than group-stage fixtures, they are still expected to fall short of the intensity and betting volumes associated with the later knockout rounds.

In addition, betting activity is highly sensitive to national team participation. Markets typically see a significant uplift in wagering when their home nation is involved, with further increases observed as teams progress deeper into the tournament. As such, overall betting volumes are heavily influenced by the performance of the largest betting markets. A scenario in which multiple major nations reach the latter stages would be expected to drive materially higher engagement, supported by increased media attention and broader consumer interest. Conversely, early exits for key markets could act as a drag on total wagering activity. As an example, France (who got to the final of the 2022 World Cup) saw 29% of World Cup wagering on the 7 matches (out of 64) in which the French team were playing.

The chart below was released by the Danish Gambling Authority, which shows the total amounts of betting stakes on each day of the World Cup (on all betting, not just World Cup betting). Unsurprisingly, those days when Denmark was playing saw a materially higher level of wagering than those days when Denmark wasn’t playing, including the final.

This chart also shows how interest peaks towards the end of the tournament. The quarter finals on 9/10 December (2 matches per day) had a higher number of wagers than in most of the days earlier in the tournament when there were 4 matches per day, and the semi-finals on 13/14 December (1 match per day) clearly show an even higher spend per game.

Global Sportsbetting Market

The chart below illustrates the global sports betting market, across both regulated and unregulated channels, which is projected to reach approximately $1.66trn in 2026. This reflects a 10-year CAGR of 14.6%, with growth accelerating in the post-Covid-19 period. Within this, Asia remains the largest market globally, ahead of Europe, while North America, Latin America and Africa have exhibited the strongest growth in recent years.

Football Estimates

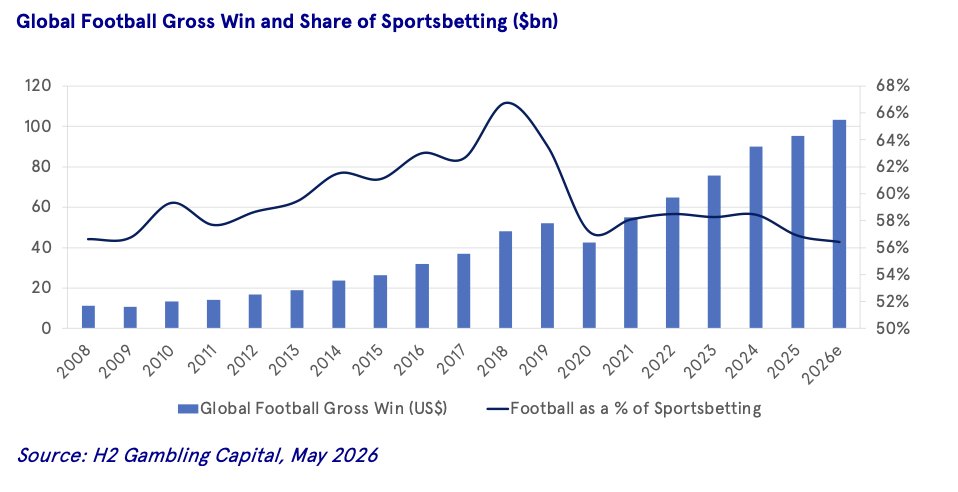

Although our sport-level split is only available on a gross win basis, global trends indicate that football betting has broadly tracked overall sports betting growth, expanding at an estimated 12.0% CAGR over the ten years to 2026.

Despite this strong growth in absolute terms, football’s share of total sports betting has declined, falling from approximately 69% in 2018 to 56% in 2026. This reflects the increasing diversification of the global sports betting market, most notably following the regulation and rapid expansion of sports betting in the United States.

Applying football’s current share of total sports betting gross win, we estimate global football turnover in 2026 at approximately $937bn, reflecting both legal and illegal channels and therefore not directly comparable to H2’s World Cup handle estimate of $60bn, which reflects legal channels only.

For illustrative purposes, we apply a hold rate of 12.5%, consistent with H2’s estimate of the global football betting margin and broadly supported by observed tournament data. France's ANJ reported an implied hold of approximately 11.7% during the 2022 World Cup; our estimate of 12.5% reflects the continued growth of parlay and bet builder betting since 2022, which carries materially higher margins than straight match wagers. Applying this rate to our World Cup handle estimate yields an estimated gross win for the tournament of approximately $7.5bn.

Conclusion on Risks to Estimates

While the expanded tournament creates additional opportunities for operators to drive engagement, we remain cautious in our handle estimates, reflecting the potential dilution in match quality and interest associated with the increased number of fixtures.

Our handle projections are also sensitive to the performance of the largest markets, both in footballing and betting terms, with deeper runs by major nations expected to drive materially higher wagering activity. Notably, Italy’s failure to qualify for the 2026 tournament represents a downside risk to European estimates; Italy is one of the largest football betting markets in Europe, and its absence from the tournament reduces the potential for home-nation-driven engagement uplift across the competition.

Gross win outcomes will, in turn, be influenced by the performance of favourites, as well as, to a greater extent than in previous tournaments, the outcomes of popular player and match-level props. This reflects the continued growth in single-game parlays (or bet builders), which have become an increasingly important driver of operator revenues.

Estimates presented in this report do not incorporate prediction markets. While we recognise their growing popularity in the United States, particularly across domestic sports, we do not expect these platforms to have a material impact on global football betting handle for the 2026 World Cup.

About H2 Gambling Capital H2 Gambling Capital is the most trusted provider of global gambling market data and intelligence. H2's proprietary research is the most widely cited source in company reports, regulatory filings, and transaction documentation across the gambling industry.